Anti-money-laundering (AML) checks are used by bookmakers and casinos to verify that gambling funds come from legitimate sources.

If you’ve ever been asked for bank statements, payslips or proof of income, you’ve likely gone through part of this process already.

In this guide, we’ll explain what AML checks are, why bookmakers perform them, how they differ from KYC and affordability checks, and what can happen if you refuse to provide documents.

My aim is to make a rather confusing topic simple and easy to understand…

Quick Answers

- What are gambling AML checks? AML (anti-money-laundering) checks verify that gambling funds come from legitimate sources.

- Are AML checks legally required? Yes. UK operators are legally required to carry them out.

- Do AML checks differ from KYC or affordability? Yes. KYC checks identity, AML checks your funds, and affordability checks look at spending sustainability.

- What documents might be requested? Usually ID, proof of address and evidence showing where your money came from.

- Can I refuse to provide bank statements? You can say no, but the bookmaker may restrict or close your account if it cannot complete its compliance checks

What Are Anti-Money Laundering Checks in Gambling?

AML checks are used by betting companies to detect suspicious transactions and verify that gambling funds come from legitimate sources. If an operator believes there is increased risk, it may ask for financial documents, monitor account activity or investigate unusual betting patterns.

In the UK, betting companies use these checks to help prevent money laundering and comply with gambling regulation. This can include reviewing deposits, withdrawals, and income patterns to ensure money is coming from legal places (not crime).

Why Do Bookmakers Perform AML Checks?

Bookmakers perform AML checks because they are legally required to prevent money laundering and other financial crime. UK gambling regulations require operators to monitor customer activity, assess risk and investigate suspicious transactions. It’s part of their licensing conditions.

These checks also protect the bookies themself. Large deposits, unusual withdrawals or anonymous payment methods all raise red flags. By requesting documents and reviewing account activity, they reduce the risk of being used for cleaning criminal finance.

Are AML Checks a Legal Requirement?

Yes. In the UK, AML checks are a legal requirement for licensed betting brands. Operators must verify customers, monitor transactions and report suspicious activity to authorities when necessary.

The Gambling Commission actively enforces these rules, and operators can face major fines or licence action if they fail to carry out proper checks.

AML rules are also influenced by wider European anti-money-laundering laws.

These regulations require extra checks for higher-risk customers, large transactions and politically exposed persons.

AML vs KYC vs Affordability Checks: What’s the Difference?

Confusingly, there are three overlapping yet distinct types of verification used by betting sites: AML checks, gambling KYC checks and affordability checks.

| Check Type | Purpose | Typical Documents |

|---|---|---|

| AML (Anti‑Money‑Laundering) | Identify the source of your funds and wealth to prevent criminal proceeds entering the gambling ecosystem. | Bank statements, payslips, tax returns, proof of asset sale or inheritance. |

| KYC (Know Your Customer) | Verify your identity, age and residency to prevent underage gambling and fraud. | Passport, driving licence, national ID, utility bill, council tax bill. |

| Source of Funds (SoF) | Confirm where the money used for a specific deposit or transaction comes from. Is it your salary, savings, or a one‑off sale? | Bank statements showing income, payslips, invoices, proof of sale (car/house), gambling winnings. |

| Affordability Checks / Source of Wealth (SoW) | Assess whether your level of gambling is sustainable relative to your overall wealth and income. Introduced to protect vulnerable customers. | Similar documents to SoF plus employment details, mortgage statements, investment portfolios. Your open banking data may be requested but is not mandatory. |

In simple terms, KYC confirms your identity, AML checks where your money came from, and affordability checks assess if you’re being responsible.

What Triggers a Money Laundering Check?

AML reviews are typically risk‑based. Bookmakers use automated risk scoring systems to flag accounts that warrant deeper scrutiny.

The most common triggers include:

- Large or unusual deposits/withdrawals – A sudden injection of funds or regular deposits disproportionate to your normal activity.

- High‑value wins or withdrawals – Withdrawing substantial winnings can prompt the operator to confirm the funds aren’t being used to launder money.

- Use of high‑risk payment methods – Pre‑paid cards and vouchers are considered higher risk because they can be anonymous.

- Multiple payment accounts – Frequently switching between different cards or e‑wallets may raise suspicion.

- Unusual betting patterns – Low‑risk high‑spend strategies (e.g. backing both red and black at roulette) or depositing and withdrawing without gambling.

- Politically exposed persons (PEPs) or high‑risk geographies – Customers from jurisdictions with weak AML controls or individuals in public office face extra scrutiny.

Some operators also use fraud-detection tools like IE Snare and device fingerprinting systems to identify linked accounts or unusual account behaviour. Betting companies change their risk thresholds as regulations evolve.

Do Big Wins Trigger an AML Review?

Large wins can sometimes trigger AML reviews, especially if the withdrawal is unusual compared to your normal betting activity. Bookmakers may ask for proof of funds to ensure the account is not being used for money laundering.

If your deposits and betting history are consistent, the process is usually stress free. Sudden large deposits followed by a big withdrawal are more likely to attract additional checks.

What Does Suspicious Activity Mean in Betting?

Suspicious activity is behaviour that may suggest money laundering or other financial crime.

The Gambling Commission highlights several betting patterns that trigger additional scrutiny, including:

- Making large bets relative to known or estimated income

- Depositing and withdrawing without playing

- Using multiple payment methods or third‑party accounts

- Patterns designed to minimise risk, such as covering both sides of an outcome

- Frequent use of anonymous pre‑paid cards

- Attempting to circumvent limits or using different identities.

If suspicious activity is detected, the operator may file a Suspicious Activity Report with the National Crime Agency. This can lead to temporary account restrictions or withdrawal delays while checks are completed.

Importantly, this does not automatically mean you have done anything wrong. In many cases, the bookmaker is simply following its legal obligations.

Source of Funds v’s Source of Wealth…

It’s important to understand the difference between source of funds and source of wealth. Source of funds refers to where the specific gambling money came from, while source of wealth looks at how your overall wealth was built over time.

For example, SoF might involve proving a £5,000 deposit came from salary, savings or a property sale. SoW checks are broader and can include tax returns, business income or inherited assets. Bookies will usually start with source of funds checks before requesting deeper financial information.

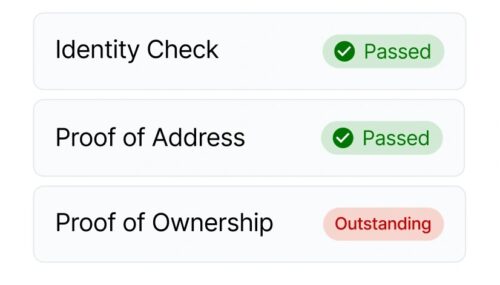

What Documents Can Be Requested?

The documents requested depend on the risk level and the specific check type.

For basic KYC, you’ll need to provide:

- Photo ID: passport, driving licence or accepted ID cards.

- Proof of address: utility bill, bank statement or council tax bill.

For AML and SoF checks, you may be asked for:

- Recent bank statements showing regular income

- Payslips or salary statements

- Proof of sale of assets (e.g. car sale invoice, property completion)

- Inheritance documents or trust statements

- Tax returns or business accounts for self‑employed individuals.

Remember that operators must adhere to the GDPR and data minimisation principles. They should only collect the data necessary for the specific purpose and retain it for a minimum period (usually five years) required by AML regulations. You can ask why each document is needed and how it will be stored.

What Happens if You Refuse AML Checks?

Refusing to provide the requested documents is within your rights, but it has consequences. The operator must balance customer privacy with legal compliance.

If you decline to supply proof of funds, they may:

- Restrict or suspend your account

- Return your remaining balance but refuse future deposits or bets

- File a suspicious activity report if they suspect money laundering

Refusing checks can sometimes lead to temporary suspensions, withdrawal delays or wider account restrictions while the operator completes compliance reviews.

The Gambling Commission requires operators to deny services to customers who cannot satisfy AML requirements. While this may feel intrusive, it’s the only way bookmakers can remain compliant. To protect your rights, request information on how your data is processed and stored, and consider providing redacted documents that still demonstrate the necessary information.

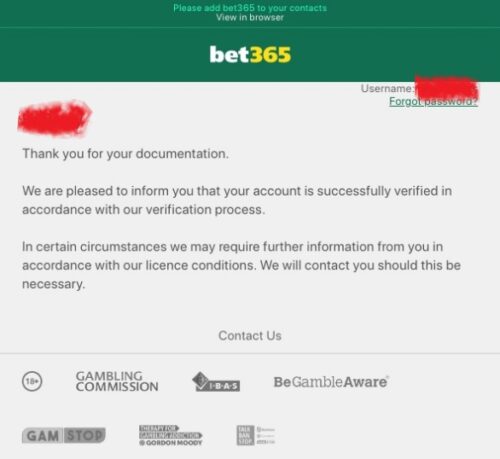

How Long Do AML Checks Usually Take?

The duration varies widely. A simple KYC or SoF review might be completed within a few hours if your documents are clear and your betting pattern is straightforward. Enhanced due diligence could take several days or even weeks, especially if additional documents are required or if the operator must wait for guidance from law enforcement. During this time, withdrawals may be frozen.

My advice to minimise delays is:

- Submit clear, legible documents in common formats (PDF or JPG)

- Ensure your name and address match the details registered on your account

- Provide redacted statements that still show income and relevant transactions

- Respond promptly to any follow‑up questions from the compliance team

Keeping your gambling activity structured, sustainable and documented can also help avoid unnecessary scrutiny — especially if you already follow sensible responsible gambling strategies.

Your rights and Data Privacy Regarding AML

Even though operators must comply with AML laws, you still have rights under data protection regulations. The UK GDPR and Data Protection Act require operators to process your personal data lawfully, fairly and transparently.

They should only collect what they need and retain it for as long as necessary for regulatory purposes. If you wish, you can find out what information they hold on you via our subject access request template here.

You have the right to:

- Request access: Ask what data the bookmaker holds about you and how it’s used.

- Rectify errors: Correct inaccurate or incomplete data.

- Object to processing: In some cases, object to how your data is used.

- Erase data: Request deletion of your data when it’s no longer required.

- File a complaint: If you believe your data is mishandled, complain to the bookmaker’s Data Protection Officer or to the UK Information Commissioner’s Office.

Frequently Asked Questions (AML)

What triggers an AML check on a betting account?

High deposit volumes, large withdrawals, irregular betting patterns or use of anonymous payment methods can trigger a review.

Is AML the same as KYC?

No. KYC verifies your identity and age, while AML investigates the origin of your funds and wealth.

Why are bank statements required?

Bank statements demonstrate where your gambling funds come from and help detect suspicious activity.

Do small bettors undergo AML checks?

Not usually. AML reviews are risk‑based. However, affordability checks might still apply at lower thresholds (£150–£500 per month).

Will my data be shared?

Operators may share your data with regulators and law enforcement. They must inform you about data processing and comply with GDPR.

Our Final Conclusion:

Anti‑money‑laundering checks are here to stay. While they can feel intrusive, they protect the betting ecosystem from criminal abuse and help regulators ensure gambling remains fair and safe.

Understanding the differences between AML, KYC and affordability checks, and preparing the right documents, will make the process smoother. As customers become more aware of their rights and operators refine their communication, we hope to see a more transparent and user‑friendly approach to compliance.